One day last April, I met Mark and Sarah (not their real names) at a McDonald’s down the block from their apartment, in Glenbrooke North, a mixed-income neighbourhood in New Westminster, British Columbia. The restaurant is kitty-corner from a nondescript mini-mall. A government-subsidized seniors’ complex and a BC Housing project are nearby. Mark appeared in a black hoodie, riding an electric wheelchair. At thirty-nine, he has trouble walking due to muscular dystrophy. His wife, Sarah, followed. Six years his junior, she does not outwardly show the ravages of fibromyalgia, which have forced her into experimental drug therapy. Both are on government disability. Sarah hasn’t had a job since the call centre where she used to work closed five years ago. Mark hasn’t worked since 2007.

Like 96 percent of Canadians, they have a bank account—a requirement for the automatic deposit of their monthly disability cheque, which totals just over $1,500. But, for all other financial needs, their current lifeline is the Money Mart in the mall across the street. At this tiny payday-lending store wedged between an insurance broker and an M&M Meat Shops franchise, the couple regularly put money onto a reloadable debit card and take out small short-term loans at annual interest rates in the triple digits. In theory, such advances are designed to tide customers over until their next paycheque arrives, at which point the entire debt is settled. In exchange for a postdated cheque or pre-authorized debit for the principal, plus fees, customers in BC can walk away with up to 50 percent of their next payday in hand.

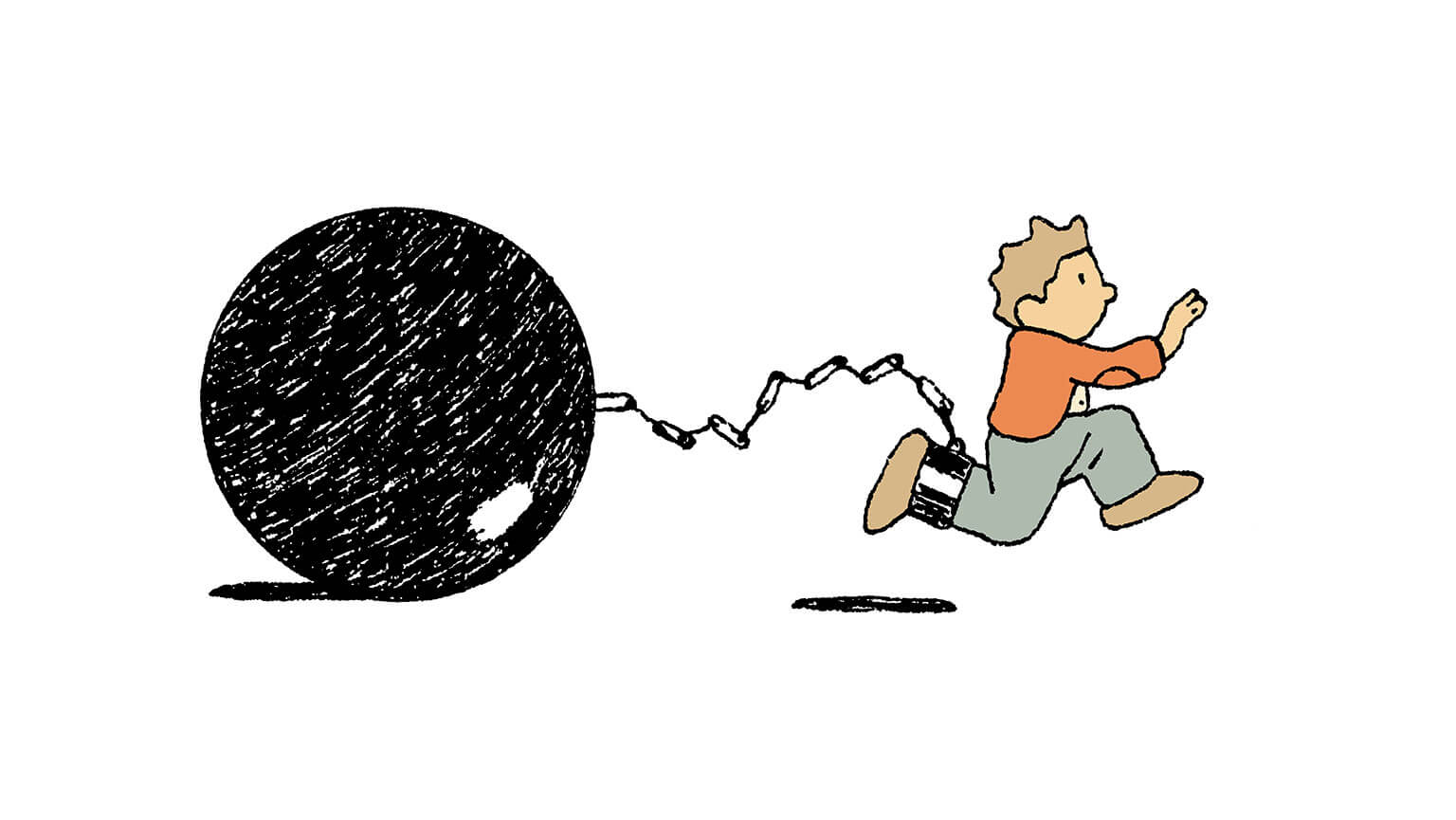

In practice, however, that’s not always how it works. For Mark and Sarah, the last five years have been defined by regular sprints on the payday-loan treadmill—a metaphor, widely used by critics of the industry, that conjures the image of a gerbil trapped on a wheel. (Although they don’t have jobs, their disability benefit qualifies as a paycheque.) Typically, each $200 to $300 they borrow triggers a crisis. They are able to pay the money back, plus fees—about $46 for a $200 loan, $69 for $300—at the end of the month, but to eat and pay rent in the following month, they must borrow more on the spot. Describing the couple’s payback strategy over coffee at McDonald’s, Mark sounded like an addict self-administering a reduction cure: they taper down the amount re-borrowed each month, pay it in full, and combine their GST cheque with money borrowed from their families eventually to pay off the debt entirely.

When I checked in with Mark again in December, he assured me they would pay off their latest loan by the end of January. “Two hundred dollars is not a lot of money, which is why banks won’t loan us that much,” he said. “But, for us, it’s the difference between eating and not eating this month, or having a place to live and going to a shelter.”

The couple is among the more than 198,000 British Columbians who took out a combined 858,000 payday loans in 2014. Every year, 2 million Canadians turn to such businesses, drawn by convenience, anonymity, or the fact that there is simply nowhere else to go. Since payday lenders first appeared in Canada in the mid-1990s, at least 1,770 storefront operations have sprung up across the country. They differ from traditional banks in that they are regulated provincially rather than federally, do not take customer deposits, and draw revenue primarily from the extremely high interest they charge. The industry has emerged because a market exists for its services—particularly small loans ranging from $100 to $1,500 that can be turned around quickly and without a conventional credit check. But, in serving this market, are payday lenders preying on vulnerable, low-income Canadians?

Using future paycheques as collateral for loans dates back at least to the American Civil War, when shady entrepreneurs followed Union armies from battlefield to battlefield, advancing funds to impoverished soldiers in exchange for a cut of their future earnings. Around this time, as industrialization drew more and more workers to urban centres, salary lenders began to appear in eastern US cities, providing advances at interest rates exceeding 500 percent a year. While these lenders never migrated as far north as Canada, pawnbrokers did, which allowed people who could pledge some form of security to access short-term loans. Meanwhile, beginning in 1906, the Canadian government passed a succession of usury laws to protect consumers. Banks began to lend small amounts, and consumer-finance companies soon appeared to grant modest loans, typically charging interest in the range of 28 to 35 percent per year on monthly payment plans designed to fit clients’ budgets.

The boom that followed World War II, along with the emergence of new technologies, changed the way everyone, rich and poor, thought about borrowing. In the ensuing decades, mainstream financial institutions began to offer credit cards, overdrafts, and lines of credit. Meanwhile, plentiful jobs and an increase in disposable income enabled the rebranding of debt—an age-old scourge—as credit. “Most of our grandparents grew up in a time when you had to be fiercely independent and look after yourself,” said Scott Hannah, president and CEO of the Credit Counselling Society, Canada’s biggest nonprofit debt-counselling service. “With no pension plan or safety net, you had to save, and when something broke, you fixed it. These lessons were not passed on.” In the span of a generation, many Canadians went from relying on savings for emergencies to relying on credit.

In the 1980s, with the popularization of credit cards, which were much cheaper to administer, North American banks largely abandoned small loans. For those who could not access conventional credit—including new immigrants, young people without established credit ratings, and those who were bankrupt but still employed—something new emerged. James Eaton of Johnson City, Tennessee, was a veteran of the credit-bureau business, gathering consumer information and selling it to lenders. In 1991, he opened a retail store called Check Cashing Inc. While his principal business was cashing paycheques without the delay of a bank hold, charging 2 to 3 percent for the service, Eaton also started offering small loans and accepting future paycheques as collateral.

At first, this was simply considered another form of cheque cashing, according to economist and author John Caskey of Swarthmore College, in Pennsylvania. He believes the concept likely emerged when a financially pressed customer came to their regular cheque casher and asked for an advance in exchange for a personal postdated cheque. With a payday just around the corner, the customer was good for it—and was willing to accept high interest to get out of a pinch. Then as now, the service was not geared toward the very poor. It always has been marketed to low- and moderate-income households—albeit those with few savings and limited access to credit. “In many cases, their customers have severely impaired credit histories, or they have reached their limit on lower-cost sources of credit, such as credit cards,” Caskey said.

Tapping this market—people with steady but low-paying jobs, bad credit, and a willingness to pay triple-digit annual interest—proved highly profitable. The relaxation of state usury laws in the 1980s allowed the industry to flourish across the South and the Midwest. In many states, the annual interest-rate cap, which was typically around 36 percent, was either raised or eliminated altogether. In the early 1990s, according to an article in Harper’s magazine, there were fewer than 200 storefronts in the US offering such loans; by 2005, there were more than 22,000.

Canada’s era of payday lending began in 1996, when the Pennsylvania-based Dollar Financial Group Inc. (now known as DFC Global Corp.) bought Money Mart, an Edmonton chain. Money Mart started in 1982 and had grown to more than 180 outlets across the country by the time Dollar Financial swooped in. Like similar companies in the US, it was initially a cheque casher before it embraced payday loans. In the late 1990s and early 2000s, many new Canadian companies followed it into the business, including Instaloans, Cash Store, Cash Money, and hundreds of mom-and-pop operations. Between 1999 and 2005, the number of outlets increased by 149 percent in Toronto, Vancouver, and Winnipeg, growing from six to forty-three branches in Winnipeg alone. In 2007, Profit magazine deemed Cash Store Financial the country’s fastest-growing company, with five-year revenue growth of 33,700 percent.

The industry thrived in a regulatory vacuum. Successive federal governments refused to enforce a 1980 usury law that made it a criminal offence for lenders to charge more than 60 percent annual interest. By law, credit cards must present interest in terms of an annual percentage rate, or APR—a single number that represents how much borrowers would owe if they didn’t pay their debts for an entire year. Interest rates on payday loans, however, can be confusing. A $23 fee on a $100 two-week loan—the current cap in BC—seems, at first glance, to indicate an interest rate of 23 percent. But expressed in credit-card terms, it is close to 600 percent APR.

Scott Hannah calls the period roughly between 1996 and 2007 the “Wild West” era for payday lending in Canada. “We saw that the interest rates charged, including certain fees, in many cases were at or near 1,000 percent,” he said. He told me the story of a BC man who borrowed $100, then paid $25 every two weeks to “roll over” the loan—that is, borrow the same funds again, with added fees—because he could never scrape together enough money to pay off the debt entirely. This went on for two years before the Credit Counselling Society stepped in and negotiated with his lenders.

According to Olena Kobzar, a social sciences professor at York University, in Toronto, who wrote her dissertation on the industry, payday loans arose as part of a wider group of “subprime” financial products. These included automobile title loans—in which a vehicle title serves as collateral—and, notably, the toxic mortgages that fed the 2008 financial crisis. The common thread through these products is that money was lent to ever-riskier groups of people, which justified charging much higher interest rates. In the case of payday loans, rates sometimes exceeded those offered by mafia syndicates. In her dissertation, Kobzar cites a study that compared the rates charged by US payday lenders at the turn of the twenty-first century with those charged by loan sharks throughout history. Typical payday-lending rates, at 450 percent, were much higher than the latter’s average of 250 percent. “Why is the larger rate deemed to be legally acceptable,” Kobzar writes, “while the lesser rate is designated as criminal? ”

When I met Desiree Wells on Granville Street in Vancouver, the November chill hadn’t stopped her from wearing a low-cut T-shirt that revealed a sweeping tattoo across her upper chest: giant bat wings surrounding a heart, flames, and the word disarray in blue India ink. (She explained that it’s a play on her name.) Wells lives in Langley, a distant suburb, but had come downtown for a marketing focus group—an easy $100 in cash just to talk about cider and coolers, with some free samples thrown in.

To a bank or credit union, Wells represents a high-risk case. That makes her a member of the captive financial underclass that payday lenders, depending on one’s point of view, either serve or exploit. She grew up in Kitchener, Ontario; after graduating from high school, she worked for a credit-card company, which provided her with easy access to many different cards. Before long, she had maxed them out. She took out her first payday loan in 2000 to make ends meet while working at a Subway. “I’ve used every single company, and they all suck,” she said. “It’s a trap, and once you’re in, it’s so hard to get out.”

After a succession of service jobs, Wells left Ontario for BC in 2012 and worked for two years as a nanny. About a year ago, she went to a payday lender to cash a cheque and learned that she owed more than $6,000 from unpaid loans. She now is applying to get on disability (she uses a prosthetic foot) and still is unemployed, relying on friends and her boyfriend’s family for help. She doesn’t know how she will get out of debt. “Unless I win a lottery, I won’t,” she shrugged. “Realistically, it’s not gonna happen.”

When regulations finally came to the payday-loan industry, they were prompted not by the federal government enforcing the Criminal Code but by disgruntled customers like Wells. One day in 2002, a courier named Kurt MacKinnon, who regularly made deliveries to the downtown Vancouver office of the boutique law firm Hordo & Bennett (now Hordo Bennett Mounteer), complained to a legal secretary about the fees charged at the lenders he used, including Money Mart. “Looking at it, we realized that if Money Mart’s practices were unlawful, as alleged, then it was likely that the practices of the entire industry were unlawful,” said HBM managing partner Mark Mounteer.

In January 2003, the firm launched an industry-wide class-action suit against Money Mart and every other payday lender in the province. The BC Supreme Court rejected this approach but allowed HBM to pursue class actions against individual companies. So in 2005, the firm shifted gears, dropping all defendants except for Money Mart, which, by that time, had become Canada’s biggest payday lender. This was the first of at least twenty-five class actions the firm brought against companies in BC, Alberta, and Manitoba—and the floodgates opened. Actions across the country targeted many of the largest companies, as well as a number of smaller chains and independents. The basis of these suits was always the same: all fees charged in excess of the Criminal Code interest limit of 60 percent were illegal.

The class actions revealed the lengths to which payday lenders would go to get around federal law. Mounteer said one company gave out loans at less than 60 percent interest but made it mandatory for a delivery service to drop off the money for a $20 fee. Another employed a brokerage model: a staffer would present himself to clients as a middleman whose job it was to locate a loan for a fee; once hired, the same employee donned a new hat as a lender, dispensing the funds with new costs attached.

The actions also forced the larger companies, which banded together in 2004 as the Canadian Payday Loan Association, to confront the fact that many of their dealings were unlawful. This threatened their very existence. They needed to convince the government to change the rules.

At the height of the Wild West era, Stan Keyes found himself out of a job. A former broadcast reporter for CHCH TV, in Hamilton, Ontario, Keyes was first elected as a Liberal member of Parliament in 1988 and later took on multiple ministerial portfolios, including National Revenue, under Prime Minister Paul Martin. He was stationed in Boston and enjoying a plum diplomatic position when Stephen Harper was elected in 2006. As Canada shifted from Liberal red to Tory blue, Keyes was dropped. He thought about taking a year off to relax, but a friend from FleishmanHillard, the US public-relations giant, called to say the CPLA wanted to hire him as its president. Keyes accepted. At the time, he said, the industry was entrenched in two camps: there were the shady, fly-by-night players and the more sophisticated members of the CPLA. The latter, initially made up of about fifty companies, understood that embracing some regulation was the only way the industry would survive. His job was to lobby on their behalf.

Regulating the industry meant convincing the federal government to change the section of the Criminal Code that made payday loans illegal. The CPLA and FleishmanHillard launched a nationwide media and government lobbying campaign. In October 2006, then justice minister and attorney general Vic Toews introduced Bill C-26, which received royal assent the following May. The bill changed the Criminal Code to exempt payday lenders from criminal sanctions, provided that provinces enacted their own regulations. “Overall Bill C-26 was a victory for the payday loan industry in Canada,” writes Nathan Irving in the Manitoba Law Journal. “It conferred legitimacy on the industry while allowing payday lenders to continue charging exceptionally high interest rates.”

In the years since, six provinces have enacted their own legislation and received Ottawa’s approval; Prince Edward Island and New Brunswick are taking steps to do so. At the low end, Manitoba now caps prices (including fees) at $17 for every $100 borrowed; at the high end, Nova Scotia’s cap is $25 per $100. Newfoundland, Quebec, and the territories have not created their own regulations. In Newfoundland and Labrador, the federal usury limit of 60 percent still applies, although this has not stopped the industry from operating there. Quebec has its own 35 percent annual-interest cap, which makes it uneconomical for lenders to offer payday loans. But Money Mart still operates a Quebec chain of cheque cashers, Insta-Cheques, which offers many of its other services.

The regulations have put a stop to many of the industry’s worst abuses. All provinces with regulations have established lending caps for individual customers and outlawed the kinds of rollovers that kept Scott Hannah’s client paying off his $100 in perpetuity. Under BC’s rules, established in 2009, if a customer cannot pay back a loan by his or her next payday, the company can thereafter charge only 30 percent annual interest on the outstanding principal and a one-time fee of $20 for a dishonoured cheque or pre-authorized debit. Lenders in BC and some other provinces are also now required to display the cost of an advance both as a flat fee and in APR. “When I started, in 2006, it was a Wild West for the industry,” said Keyes. “Now we are legal, licensed, and heavily regulated.” Still, customers continue to have difficulty escaping the treadmill. According to Consumer Protection BC, about a quarter of the loans given out in 2014 “initially defaulted,” meaning many borrowers were unable to come up with the money by their next payday and were forced to pay additional fees.

The industry still runs into legal trouble. In 2013, with Ontario regulators planning to revoke the Cash Store’s payday-lending licence due to alleged violations of the law, the company said that it would start offering lines of credit instead. But the following year, the Superior Court ruled that these were effectively payday loans, and in February 2014 provincial regulators said they would refuse to renew the Cash Store’s licence. Deprived of its biggest market, the company entered bankruptcy protection. Money Mart now is poised to take over an undisclosed number of Cash Store locations—meaning Canada’s biggest chain, with more than 500 stores, is about to become even bigger.

Numerous class-action lawsuits continue. Mark and Sarah were part of the first against Money Mart, which was settled in 2010 for $24.75 million, but the way they were reimbursed for the illegal fees they paid all those years ago remains a sore spot. Initially, the couple was ecstatic to hear they would get more than $400 back. However, they soon learned that the settlement would be split into two tranches. The first would be paid out in cash, with an option to get the second half immediately—in the form of Money Mart vouchers for future services. If they wanted the second payment in cash, they would have to wait three years. They resolved to do so. In July 2014, eleven years after the action started, Sarah walked into the local Money Mart. She had to argue for a half-hour, but eventually she came out with a cheque.

In the late 1990s, Rob Della Malva was working multiple jobs—towing cars, driving a cab—while struggling to launch an automotive-repair business. A Montreal native living in Surrey, BC, he started dabbling in payday loans to avoid the embarrassment of having to borrow from family. At first, he had no problems, but as he borrowed ever-larger amounts, he found himself unable to pay the principal back each time and was forced to roll over his existing loans while taking out new, concurrent ones. At one point, he was indebted to three companies, paying off one to reimburse another. He was soon $25,000 in debt—a figure that includes money he borrowed from a consumer-finance company—and was unable even to pay off the interest. “I started seeing a trend,” he said, “and the trend was I was never going to pay this off.”

In the language of Money Mart’s parent company, DFC Global Corp., Della Malva is an ALICE: asset limited, income constrained, employed. DFC’s website defines an ALICE as a small-business owner or service worker who typically holds more than one “lower-paying job” to meet bills and expenses. ALICEs are prized because they are repeat customers. Confronted by growing living expenses but with inadequate income and no hard assets, many have no choice but to return to lenders. (The company’s other target is ARTI customers—asset rich, temporarily illiquid—who use its network of pawnshops.) DFC estimates there are at least 150 million ALICEs like Della Malva living in the ten countries in which the company operates. “As a result of stagnant wages and rising prices for goods and services, we believe the number of ALICE and ARTI people are increasing,” reads a DFC web page for investors.

Della Malva’s insomnia grew worse in proportion to the size of his debts. His irritability alienated family and friends. Fearful of creditors, he screened his calls. In December 2013, he reached out to the Credit Counselling Society by email because he was too embarrassed to phone. After an evaluation of his existing debt, assets, and income, the nonprofit contacted his creditors and set up a single consolidated payment each month. At this pace, the debt will be gone in 2016. He now is convinced the industry must be better regulated. He believes that, in addition to lowering the interest they charge, companies should not be allowed to loan a customer half of their next paycheque. “When you’re only making 500 or 600 bucks a week,” he said, “that’s crazy.”

Della Malva is not alone in his thinking. Among the most vocal advocates for change in Ontario and British Columbia—the two provinces with the most lenders—is the 70,000-member social-justice group Association of Community Organizations for Reform Now (ACORN). In late January, I attended an ACORN demonstration outside a new Cash Money outlet on Kingsway in Burnaby, BC. About twenty activists converged on the sidewalk to protest the opening of the store, just two blocks away from a Money Mart. ACORN has been pushing the city to create a zoning bylaw that would limit the clustering of payday-loan businesses in low-income neighbourhoods. (Surrey passed a similar bylaw in April 2014.) It’s this proximity, an organizer named Scott Nunn told me, that results in the kind of concurrent lending to which Della Malva and others have fallen victim. “Payday lending is symptomatic of a larger problem,” he said. “Do you think if the cost of living was addressed through raises in wages and the disability and assistance rates people would still be going to places like this to get payday loans? ”

ACORN’s main demand is that BC lower interest rates. Activists point to Manitoba’s current cap as proof that it can be done. To limit the most predatory aspects of the industry, they call for several other measures: the creation of a database that would allow lenders to screen out customers with existing debts; a loan limit not to exceed 25 percent of a borrower’s next payday; and more time to pay than the typical two weeks.

The provincial government seems to be listening, at least in part. During the last election, in 2013, Premier Christy Clark campaigned on a promise to lower the cap to $17 from $23. She was reelected, and the government maintains it will follow through as part of a wider review of the regulations. Meanwhile, Ontario and some other provinces have either started reviewing their regulations or are planning to do so by next year. This is part of a wider national and international movement toward change. In its 2013 Economic Action Plan, the federal government promised to combat what it called “predatory lending” by payday-loan companies, and the US Consumer Financial Protection Bureau has recently proposed new measures.

Keyes warned that making regulations too strict could backfire. In BC, he predicted, lowering the cap to $17 would cause smaller companies to die and prompt larger companies to close locations and roll back services. “You are now creating a void to be filled by the unregulated online industry,” he said. “The consumer is still there and the demand is still there, but where do they turn? ”

Online payday lending, now a multibillion-dollar industry, is even more shadowy and poorly regulated than its bricks-and-mortar counterpart. In November 2014, Washington State’s Department of Financial Institutions fined Carey Brown, the Tennessee-based owner of mycashnow.com and several other sites, more than $100,000 for operating without a licence and ordered restitution to at least fourteen customers. About three months earlier, New York authorities charged Brown with nearly forty counts of criminal usury, for charging interest rates of between 350 and 650 percent. Investigators traced mycashnow.com to the tiny Caribbean island of Anguilla, where it was established as a shell company. Other online lenders have based their operations on US tribal lands to skirt state laws. Much as cheque cashers morphed into payday lenders, the move online is simply another tactic aimed at circumventing regulations, according to Paige Skiba, an economist and professor at Vanderbilt University Law School, in Nashville, Tennessee. “I’m not really optimistic about regulators finding a way to make payday lending a safe product for the majority of consumers,” she said.

On a rainy Friday night in March 2013, Tamara Vrooman, the president and CEO of Vancity, Canada’s biggest community credit union, went undercover to a payday-loan store in Vancouver. Internal research had confirmed that 15 percent of Vancity members were accessing such services on a regular basis. When she arrived, there was a lineup. Vrooman chatted with a single mom who needed cash for groceries and a well-dressed realtor who relied on reloadable Visa Debit cards—which allow customers to load a set amount of money and spend it anywhere Visa Debit is accepted—to keep his expenses from exceeding his income.

Except for the Plexiglas box encasing the single employee, it was a clean, “cheery” environment, Vrooman recalled. The staffer was young, friendly, and multilingual. The visit made Vrooman realize just how varied the industry’s clientele are, and she came to see the demand for payday services as an opportunity. Vancity decided to design a short-term loan at interest rates comparable to a typical credit card—in this case, 19 percent APR. It would be processed quickly enough to deal with sudden emergencies while still contributing to a member’s credit rating. It would require a credit check and regular income, but a member could pay it back over the course of two to twenty-four months.

In June 2014, Vancity launched Fair and Fast, offering sums between $100 and $1,500. In the first six months of the program, the credit union provided more than 700 loans, saving clients an estimated $500,000 in interest and fees that would otherwise have gone to payday lenders. The loans cost $2.38 per $100 if paid back within two months. The underlying motive of the Vancity program is to reenter a space that Vrooman feels mainstream financial institutions no longer adequately serve. “We believe the way to get economic growth is to have more people participating in the economy, not fewer,” she said.

Efforts like these need to ramp up, said Jerry Buckland, a professor of international development and the dean of Menno Simons College, in Winnipeg. “Vancity is small in comparison to the big banks, so why is it that Vancity can do this and not one of them? ” he asked. Buckland, the author of Hard Choices: Financial Exclusion, Fringe Banks, and Poverty in Urban Canada, got hooked on the subject in 2002, when he returned home from development work in Bangladesh and discovered that, in terms of access to banking services, poor neighbourhoods in Winnipeg were often worse off. Buckland believes Canada’s big banks need to do more to serve the needs of low-income people. He points to the Access to Basic Banking Services Regulations—which requires federally regulated banks to open accounts and cash some cheques for any citizen with adequate ID—as a law that needs to be expanded. “In this regulation, I think we have the seed of a really important concept,” he said.

Buckland believes more Canadians should have access to low-cost bank accounts (for transactions and savings) and small amounts of credit. Many banks and credit unions currently offer both low-fee and reloadable cards, for example, but do not actively promote them, since the profits they yield are small. (In January, eight of Canada’s biggest banks voluntarily committed to making no-cost accounts available to youth, students, and a limited number of seniors and people with disabilities.) Buckland’s research also shows that a disproportionate number of bank branches have closed in lower-income urban Canadian neighbourhoods—presumably, he writes, “because they have found these branches to be marginally or not at all profitable.”

According to Duff Conacher, a visiting professor at the University of Ottawa’s School of Political Studies, this departure set the stage for cheque cashers—and, later, payday lenders—to take hold. In some cases, they even moved into the physical storefronts vacated by banks. Since 1994, he has been pushing for Canada to create a version of the US Community Reinvestment Act, which requires banks to track and disclose the services offered in different communities, particularly ones with low or moderate income levels. Banks are subject to regular review, and the results are analyzed for patterns of withdrawal that appear to be discriminatory, including on the basis of income and race. This has prevented the closure of branches while providing an incentive for the institutions to supply basic services to low-income customers. (The NDP championed a similar law in the 1990s, but has since abandoned it.)

For its part, the Canadian Bankers Association disputes the idea that low-income Canadians are underserved. “I question the very assumption of that question,” said CBA president Terry Campbell, when I asked whether banks have an obligation to do more. The continued existence of payday lending is really an issue of financial literacy, he argued. To that end, the CBA promotes educational programs for students and seniors. For customers in credit trouble, Canada’s banks donated more than $21 million last year to non-profit credit-counselling agencies. All Canadians who qualify can access cheaper credit options, including lines of credit and low-rate credit cards. But higher-risk credit cases often don’t qualify—which forces them to turn to payday lenders. “We are in the business of making loans,” Campbell said, “to people who will pay them back.”

When he lost his call-centre job in 2007, Mark’s life changed dramatically. Although he had been with his bank for nearly thirty years, he felt abandoned after he became unemployed. “When we were working, they were throwing services at us, proactively trying to get us to sign up for lines of credit, credit cards,” he said. “But as soon as we weren’t working, they didn’t want anything to do with us.’ ”

Eventually, Mark hopes to establish a home-based business so he doesn’t have to confront public transit in a wheelchair. He has vague plans to do “voice work” for a call centre or voice-overs for video games and TV shows. When I spoke with him again in early February, his tone was hopeful and upbeat—until I asked whether his plan to be debt free by January had panned out. He and Sarah were able to pay off their debt to Money Mart as hoped, but in the last week of January, their computer crashed and they needed $100 for repairs. With no other option, they went back to borrow more. “It’s not a big deal for us,” he said. “When we get our tax return in April, we’ll use that to pay them off, and that will be that.”

This appeared in the June 2015 issue.